1. Introduction

For the modern Tribal nation, economic self-determination is the new frontier of sovereignty. Gaming provided the initial spark for many. Now, there is a shift toward “sustainable tribal economies through business diversification.” The Michigan Economic Development Corporation (MEDC) champions this shift. They see it as a calculated political move. Their goal is to ensure long-term autonomy. Building a tribal business empire is not merely about revenue. It focuses on building state-tribal relationships. These relationships foster development “beyond the casino.”

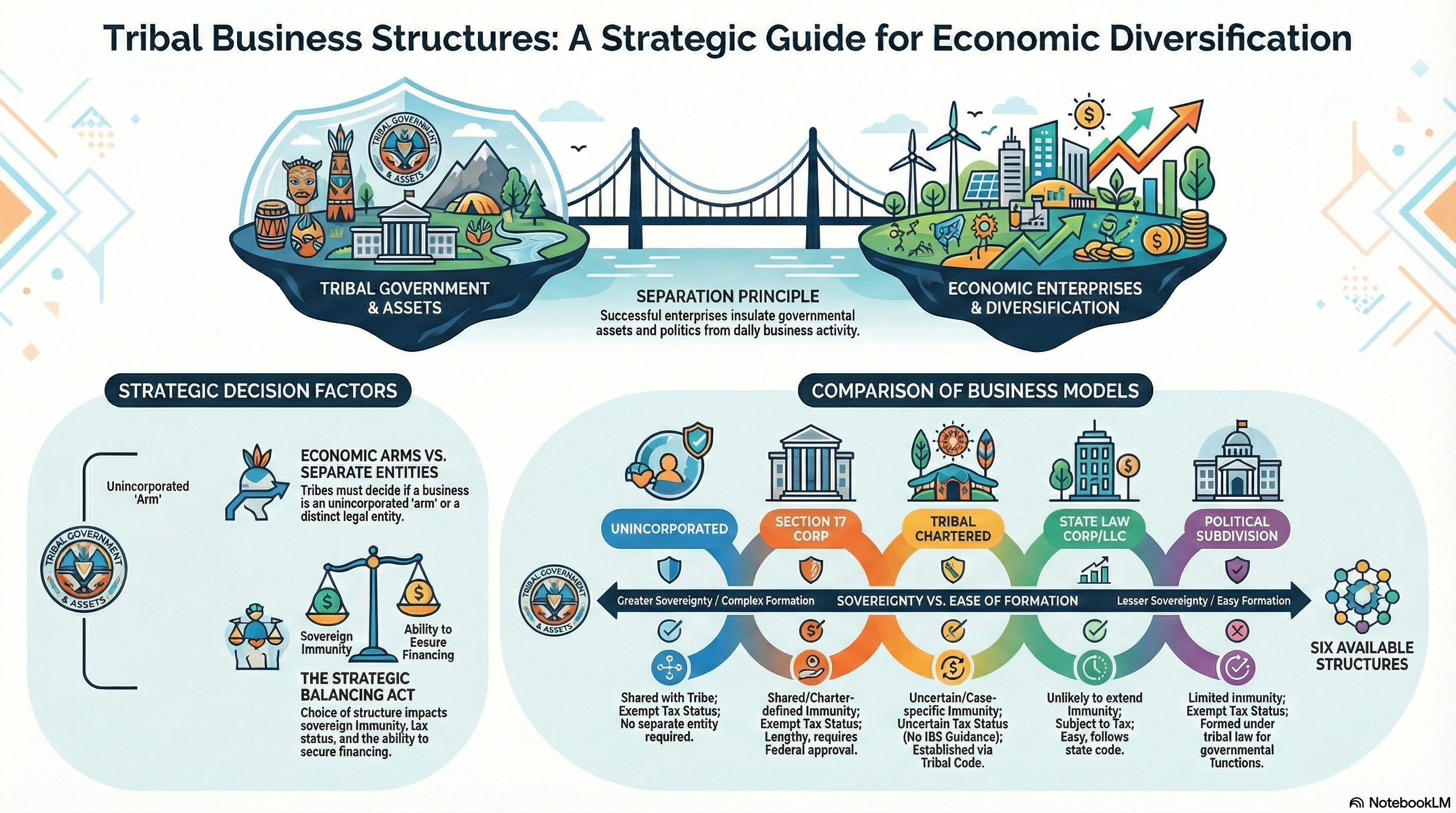

The central challenge for any Tribal leader or strategist is the “market-sovereignty” tension. Leaders need to preserve ancient sovereign rights. Simultaneously, they must satisfy the transparency and speed requirements of a globalized marketplace. To succeed, a Tribe must navigate complex legal architectures. They need to find a structure that protects its assets. This must be done without diluting its power.

2. The Sovereign Immunity Paradox: When Being “One with the Tribe” Slows You Down

Most Tribal enterprises begin as “Unincorporated Businesses” or “economic arms.” These are not separate legal entities; they are the Tribe itself. While this preserves the Tribe’s inherent sovereign immunity, it creates a strategic bottleneck. Since the business is the Tribe, managers often cannot waive immunity unilaterally. They lack the authority to sign a standard commercial contract. Every significant deal may require a return to the Tribal Council, a process that can be fatal in fast-moving markets.

Furthermore, for unincorporated arms, the “Sovereign Shield” is a double-edged sword. Because the entity is not distinct, its liabilities are the Tribe’s liabilities. If a business arm fails, the Tribe’s general treasury is at risk. Assets and obligations are often legally intermingled.

To determine if an entity is a tax-exempt “governmental instrumentality,” the IRS applies a rigorous six-factor test derived from Revenue Ruling 57-128:

- Governmental Purpose: Is the organization performing a recognized government function?

- Performance on Behalf of the Sovereign: Does it function specifically on behalf of the Tribe?

- Private Interests: Are there private owners involved, or does the Tribe maintain exclusive control?

- Control and Supervision: Is the control of the organization vested in a public authority?

- Statutory Authority: Is there express or implied authority for its creation?

- Financial Autonomy: What is the degree of financial independence and the source of operating expenses?

As the MEDC guidebook warns:

A Tribe cannot be sued without a waiver of sovereign immunity. An agreement with a Tribe cannot be enforced without this waiver either. This is a new concept to many outsiders. It creates uncertainty that may intimidate some potential investors.

The Strategist’s Solution: Sophisticated Tribes avoid broad waivers. Instead, they utilize “carve-out” waivers to limit a creditor’s recourse to specific business assets or insurance proceeds. This approach protects the Tribe’s core treasury. It also provides lenders with the security they demand.

3. Section 17 Corporations: The Federal “Secret Weapon” for Business Agility

Under 25 U.S.C. § 477 of the Indian Reorganization Act, Tribes can petition for a Section 17 Corporation. This is the “secret weapon” for large-scale development. It creates a formal separation between the enterprise and the Tribal government.

A Section 17 charter is akin to Articles of Incorporation but with significantly more weight. Its greatest advantage is its irrevocability. The charter is issued by the Secretary of the Interior and must be ratified by the Tribe. It cannot be revoked or surrendered except by an Act of Congress. This provides a level of institutional stability that state laws cannot match.

Section 17 Corporations can:

- Hold assets and property separately from the Tribal government, shielding the treasury from business risks.

- Lease Tribal land for up to 25 years. It does not require further approval from the Secretary of the Interior. This is a massive advantage for infrastructure and real estate projects.

- Serve as both the borrower and the issuer in tax-exempt bond financing.

The federal approval process is notoriously lengthy. However, the resulting “sovereign shield” allows a Tribe to engage in major commerce. This occurs without exposing the sovereign government’s political heart to commercial liability.

4. The State-Law Trap: Why Incorporating Outside the Tribe is a Risky Shortcut

When speed is the priority, Tribes often look to incorporate under state law (e.g., Michigan’s corporate codes). This is a dangerous shortcut. By choosing a state charter, the Tribe may inadvertently “waive its way” out of its most valuable protections.

As seen in Baraga Products, Inc. v. Comm’r of Revenue, courts often view state-chartered entities as agents or citizens of the state rather than sovereigns. While an “on-reservation” presence may offer some protection, once a state-chartered tribal business moves off-reservation, it is generally subject to non-discriminatory state laws and regulations (Mescalero Apache Tribe v. Jones).

| Structure | State Law Incorporation | Tribal Charter |

| Pros | High familiarity for lenders; instant formation. | Preserves immunity; establishes Tribal jurisdiction. |

| Cons | Loss of Sovereign Immunity; subject to federal/state income tax; subject to state regulation off-reservation. | Regulatory uncertainty for outside investors; requires a robust Tribal Code. |

5. The IRS “Integral Part” Mystery: Navigating the Tax Grey Zone

Section 17 Corps and unincorporated arms have clear federal tax-exempt status. Tribally Chartered Corporations exist in a legal “Grey Zone.” The IRS has listed the tax treatment of these entities as a priority for years. However, it has yet to issue definitive guidance.

There are currently three possible IRS interpretations for Tribally Chartered Corps:

- Per Se Exempt: Treated like a Section 17 Corp.

- Per Se Non-Exempt: Treated like a private, taxable state corporation.

- The “Integral Part” Test: This is the most common and complex hurdle. The IRS evaluates the “totality of the circumstances.” They focus on the Tribe’s level of control. They also consider the financial commitment to decide if the entity is an “integral part” of the Tribe.

This “uncertainty surrounding… tax immunity” is a major barrier to attracting sophisticated third-party capital. Investors often require tax clarity. However, current federal guidance cannot provide this clarity.

6. Insulating Profit from Politics: The Golden Rule of Tribal Success

The most successful Tribal nations follow a “Golden Rule”: the enterprise must be insulated from the political process. Sustainable development fails when business decisions focus on the next election cycle. This is instead of considering the next decade of growth.

Real-world successes like Ho-Chunk, Inc. (Winnebago Tribe) and Michigan’s own Waganakising Odawa Development, Inc. (Little Traverse Bay Band) serve as the “gold standard.” These models use tribally chartered structures to separate the Board of Directors from the Tribal Council. This separation ensures that the day-to-day operations remain focused on the bottom line. At the same time, it maintains Tribal oversight.

When architecting a business structure, Tribal leaders must weigh four critical criteria:

- Sovereign Immunity: To what extent should the business share the Tribe’s immunity, and how should waivers be limited?

- Tax Treatment: Will the structure trigger federal or state income and business taxes?

- Financial Opportunities: Does the structure allow for 8(a) contracting preferences or tax-exempt bond issuance?

- Timing: How quickly must the entity be operational?

As the MEDC guidebook emphasizes:

“…the goal is to create structures that provide a separation between tribal governments and economic enterprises. These structures insulate governmental assets and politics from business activity. At the same time, they retain appropriate oversight and accountability.”

7. Conclusion: The Future of Sovereign Commerce

The modern Tribal business empire is not a monolith; it is a strategic architecture. A sophisticated Tribe might utilize a Section 17 Corporation for land-based infrastructure. They might use a Tribally Chartered LLC for a joint venture. An unincorporated arm could serve for essential government services.

By carefully choosing the right legal vehicle, a Tribe creates a “Sovereign Shield” that protects the nation’s future. The defining question for the next generation of Tribal leaders is this: How will you preserve your ancient sovereign rights? How will you meet the transparency and agility demanded by a globalized marketplace? The answer lies in the precision of the architecture you build today.